A direct rollover moves your retirement funds straight from one account to another without you handling the money, making it safer and simpler. An indirect rollover gives you the funds first, and then you have 60 days to deposit them into a new account, but it involves more risks and potential taxes if not done correctly. Understanding these differences helps you choose the best option for your financial goals; keep exploring for more details.

Key Takeaways

- Direct rollovers transfer funds directly between accounts without the individual handling the money, reducing risks and complications.

- Indirect rollovers involve receiving a check, which must be redeposited within 60 days to avoid taxes and penalties.

- Direct rollovers are simpler, with no mandatory tax withholding, while indirect rollovers typically withhold 20% for federal taxes.

- Only one indirect rollover per 12 months is allowed for IRAs, making it more limited than direct rollovers.

- Overall, direct rollovers are safer and more straightforward, while indirect rollovers require careful timing and management.

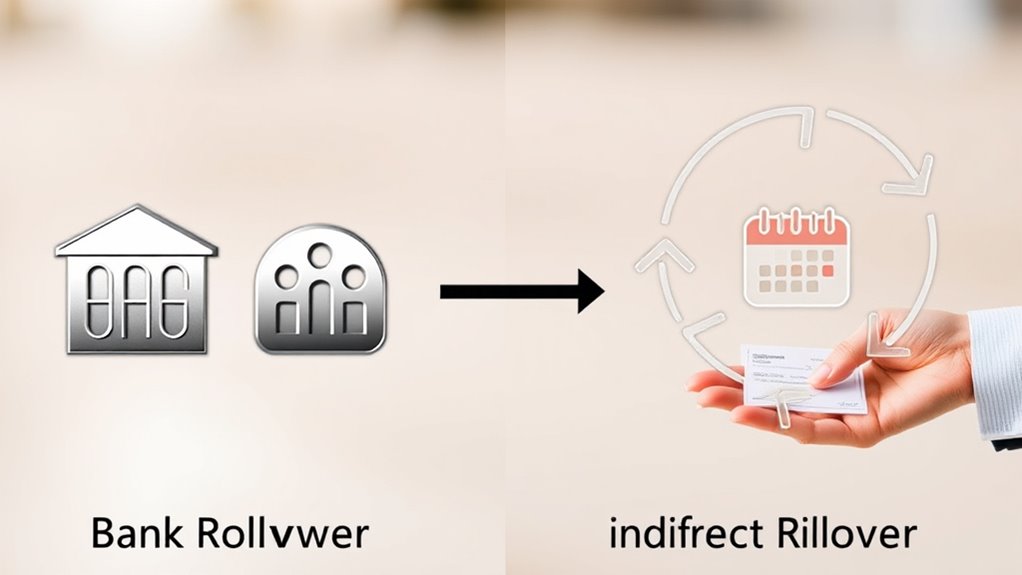

Are you considering transferring your retirement funds? Understanding the differences between a direct rollover and an indirect rollover is essential to making a smooth and tax-efficient transfer. A direct rollover involves moving funds directly from one retirement account to another without you ever taking possession of the money. This process is also called a trustee-to-trustee transfer or simply a transfer request. It’s straightforward and minimizes complications because the money never touches your hands. On the other hand, an indirect rollover requires you to receive a check payable to you first, which you then redeposit into another retirement account. You have a 60-day window to complete this redeposit to avoid taxes and penalties. If you miss that deadline, the entire distribution becomes taxable, and you could face an early withdrawal penalty if you’re under age 59½.

Understanding the key differences between direct and indirect rollovers helps ensure a smooth, tax-efficient retirement fund transfer.

When it comes to tax implications, direct rollovers are generally simpler. Since the funds move directly between custodians, there’s no mandatory federal tax withholding. You don’t have to worry about losing a portion of your money upfront. Indirect rollovers, however, involve a mandatory 20% federal tax withholding on distributions from qualified employer plans. If you’re rolling over an IRA, the withholding is usually 10%, unless you request a waiver. The withheld amount is credited against your taxes when you file, but if you don’t redeposit the full amount, you’ll owe taxes on the shortfall. This makes indirect rollovers a bit more complicated and risky if you’re not careful.

Timing is another key difference. Direct rollovers don’t impose a strict deadline for completing the transfer since the money moves directly between institutions. Conversely, indirect rollovers require you to deposit the funds into a new account within 60 days of receiving them. The countdown begins the day after you physically receive the distribution. Missing this deadline means your rollover becomes a taxable event, and you might owe penalties if you’re under age 59½. This tight window adds a layer of risk and requires careful planning. Moreover, the IRS allows only one indirect rollover per 12-month period for IRAs, which can limit your options if you need to make additional transfers within a year. It’s also important to understand that proper documentation of your rollover process can help prevent IRS complications and ensure your rollover is completed correctly.

Possession and use of funds also differ. With a direct rollover, you never possess the funds, which reduces the risk of misuse or early withdrawal. An indirect rollover puts the money in your hands temporarily, giving you flexibility to use it within 60 days. While this offers liquidity, it also means you must be disciplined to redeposit everything on time to avoid taxes and penalties. Overall, direct rollovers are simpler, safer, and less prone to mistakes, making them the preferred choice for most people. Indirect rollovers can work if managed carefully, but they come with added complexity and risk.

retirement account transfer kit

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Frequently Asked Questions

Can I Choose Both Direct and Indirect Rollovers for the Same Account?

No, you can’t choose both direct and indirect rollovers for the same account at the same time. You can perform only one type of rollover per account transfer, but you can do multiple rollovers over time if needed. If you choose an indirect rollover, you must deposit the full amount into your new account within 60 days to avoid taxes and penalties. Be sure to plan carefully to avoid mistakes.

How Do Taxes Differ Between Direct and Indirect Rollovers?

Your taxes can feel like a rollercoaster when comparing direct and indirect rollovers. With a direct rollover, taxes are mostly avoided because the money moves straight between accounts. But with an indirect rollover, if you don’t deposit the full amount within 60 days, the IRS treats it as a withdrawal, and you’ll owe income tax plus possibly a penalty. So, direct rollovers save you from surprise tax shocks!

Are There Penalties for Failing to Complete a Rollover?

Yes, you could face penalties if you don’t complete a rollover properly. If you miss the 60-day deadline for an indirect rollover, the amount may be taxed and potentially subject to an early withdrawal penalty. To avoid this, make sure you follow the rules carefully, and consider doing a direct rollover, which minimizes the risk of penalties and taxes. Always stay informed about IRS deadlines and procedures to protect your funds.

Can I Rollover a Roth IRA Into a Traditional IRA?

You can’t directly rollover a Roth IRA into a traditional IRA. These are different types of accounts with distinct tax treatments. However, you can convert a Roth IRA to a traditional IRA through a process called a Roth conversion, but you’ll owe taxes on the converted amount. Make sure to consult a financial advisor to understand the tax implications and verify you follow IRS rules for conversions.

How Long Do I Have to Complete an Indirect Rollover?

You have 60 days to complete an indirect rollover once you receive the distribution. During this period, you must deposit the funds into your new IRA to avoid taxes and penalties. If you miss this window, the amount may be treated as a taxable distribution, and you could face additional penalties. Staying aware of this deadline helps you keep your retirement savings on track and avoid unnecessary costs.

The Roth IRA Conversion Bible: Step-by-Step Guide With Numerous Examples

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Conclusion

Understanding the difference between direct and indirect rollovers helps you make smarter retirement decisions. While some worry about penalties with indirect rollovers, choosing a direct rollover minimizes that risk and simplifies the process. Remember, taking the time to comprehend these options ensures your retirement savings stay on track. Don’t let confusion hold you back—clarify your rollover choice now, and secure your financial future with confidence.

PlanNow Revocable Living Trust Kit for Individuals -Do It Yourself Revocable Trust Forms to Protect Family, Assets & Yourself – Cost-Effective with Easy Step-by-Step Instructions – Attorney-Approved

Comprehensive Asset Protection: The Revocable Living Trust forms features essential legal documents that help safeguard your family, assets,…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Retired Tool Maker Die Maker Funny Saying Retirement T-Shirt

Funny saying novelty design for retiring tool maker or toolmaker working as a die maker. Perfect for retirement…

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.