In your 30s, focus on building a solid financial foundation by maximizing retirement contributions, diversifying investments, and avoiding lifestyle inflation to leverage compound growth. In your 50s, shift to managing risks, using catch-up contributions, and planning for shorter time horizons. It’s essential to review your portfolio regularly and adjust strategies based on your goals. To discover effective ways to adapt your retirement plan at any age, explore more about these evolving strategies.

Key Takeaways

- Early 30s focus on aggressive savings, compound interest, and establishing diversified investments; 50s prioritize risk reassessment and catch-up contributions.

- In your 30s, building an emergency fund and managing high-interest debt are crucial; in your 50s, planning for healthcare and long-term care costs becomes essential.

- Retirement goals set earlier allow for sustained growth; later stages require more conservative strategies and portfolio rebalancing.

- Maximize retirement account contributions early; in your 50s, utilize catch-up options to accelerate savings.

- Strategies shift from foundational growth in 30s to risk mitigation and income preservation in 50s.

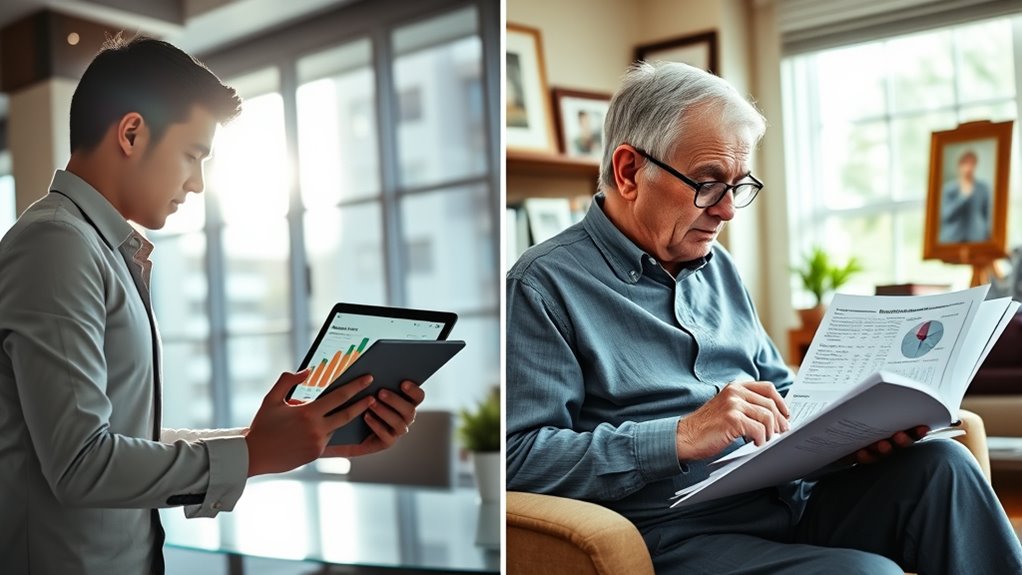

Are you wondering whether to start retirement planning in your 30s or your 50s? The answer can substantially impact your financial future, and understanding how your strategies should adapt based on your age is key. In your 30s, the main focus should be on establishing strong foundations. Early savings are essential because the power of compound interest works best when you start small but early. Contributing maximally to retirement accounts like 401(k)s or IRAs takes advantage of tax benefits and allows your money to grow exponentially over time. At this stage, diversification of investments is essential to manage risks while aiming for steady growth. Avoid lifestyle inflation—just because your income increases doesn’t mean you should boost your expenses—so you can channel more into your savings. Creating a realistic financial goal helps you stay motivated and track your progress. Setting a target, such as saving at least one year’s income by age 30, gives you a measurable milestone to work toward.

Managing debt, especially high-interest debts, should be a priority because it reduces financial burdens that could otherwise hinder your ability to save. Building an emergency fund covering three to six months of expenses provides a safety net that prevents you from dipping into retirement savings when unexpected costs arise. Regularly reviewing your financial plan ensures you’re staying on track and adjusting for changes in income or expenses. Developing good financial discipline now sets the tone for future stability. Furthermore, understanding the significance of healthcare costs as a major factor in retirement planning underscores the importance of early preparation for potential medical expenses, including insurance options and savings strategies. Incorporating inflation protection strategies into your retirement plan can help preserve the purchasing power of your savings over time.

By contrast, if you’re in your 50s, your approach needs to shift. Your focus should be on maximizing retirement savings through catch-up contributions and reassessing your investment risk level. Since you have less time before retirement, diversifying investments to balance growth potential with risk management becomes more critical. Estimating retirement expenses and planning for long-term care costs ensures you’re prepared for future financial demands. If you haven’t saved enough, explore side hustles or part-time work to boost your income. At this stage, it’s also essential to review your progress, adjust your savings targets, and plan for potential healthcare needs and other long-term costs.

Throughout both age groups, maintaining financial discipline remains fundamental. Creating a budget, prioritizing needs over wants, and avoiding unnecessary expenses help increase your savings rate. If you’re in your 50s, maximizing contributions and considering phased retirement options can smooth your transition into retirement. Ultimately, whether you’re in your 30s or 50s, adapting your strategies based on your current situation, goals, and time horizon can make all the difference in securing a comfortable retirement. Starting early gives you more flexibility, but it’s never too late to begin refining your plan and making meaningful progress toward your retirement goals.

Frequently Asked Questions

How Does Inflation Impact Retirement Savings at Different Ages?

Inflation erodes your retirement savings’ purchasing power, so it impacts different ages differently. When you’re in your 30s, inflation means you need to save more over time to keep pace with rising costs. If you’re in your 50s, inflation can threaten your savings’ value just as you’re nearing retirement, making it essential to adjust your investment strategy to hedge against inflation and guarantee your money lasts.

When Should I Consider Delaying Retirement Savings Contributions?

If you notice your savings are piling up faster than expected or your financial goals shift, you should consider delaying contributions. Maybe you’ve had a windfall or your expenses decrease, giving you extra room to save later. By delaying, you allow your investments more time to grow, especially with compounding. Just like waiting for dial-up internet to load faster, sometimes patience with contributions pays off in the long run.

What Are the Best Investment Options for Late Starters?

You should focus on high-growth investments like stocks or stock funds, which can generate higher returns over time. Consider opening a Roth IRA for tax-free growth or a taxable brokerage account to maximize flexibility. Diversify your portfolio with a mix of stocks, bonds, and ETFs to balance risk and reward. If possible, increase your contributions and take advantage of catch-up options to accelerate your savings.

How Can I Prioritize Debt Repayment While Saving for Retirement?

You should prioritize paying off high-interest debt first, as it grows faster than your savings. Once that’s manageable, allocate a portion of your income to retirement accounts like a 401(k) or IRA, even if it’s smaller initially. Automate your savings to stay consistent, and balance debt repayment with retirement contributions. This approach reduces financial stress while steadily building your future security.

What Are Common Pitfalls to Avoid in Mid-Life Retirement Planning?

You should avoid neglecting your savings, assuming retirement is distant, or taking on unnecessary debt. Overlooking investment diversification can also hurt your growth, and procrastinating on catch-up contributions limits your options later. Don’t overlook changing expenses or health needs, which can impact your plans. Keep reviewing your strategy regularly, stay disciplined, and seek professional advice if needed, to ensure you’re on track for a secure retirement.

Conclusion

So, while your 30s might seem way too early to worry about retirement, ignoring it now could leave you scrambling in your 50s. Ironically, the earlier you start, the less you’ll need to sweat later. But if you wait, you’ll realize too late that those missed opportunities can’t be made up overnight. It’s funny how procrastination now might just mean working longer later—so start planning today and enjoy your future, not just your present.